Continuing the decline that began last year as a result of rising interest rates, the real estate market continued to slow down in the first quarter of 2023, according to figures compiled by the Belgian notaries. In volume of activity but also in prices, which offers good prospects to investors who would like to enter the market today :

- The number of transactions has fallen by 7.1% compared to the first quarter of 2022.

- Putting the numbers in perspective, we can talk about a return to normalcy after the pandemic as activity remains higher in 2023 than in 2019 (+7.3% compared to Q1 2019) when rates were at the bottom then.

- In March, activity fell only 1% year-over-year, after -10.5% and -10.4% in January and February respectively.

- The number of mortgages granted by banks fell by 47.9%, mainly due to the virtual disappearance of refinancing files (Febelfin figures).

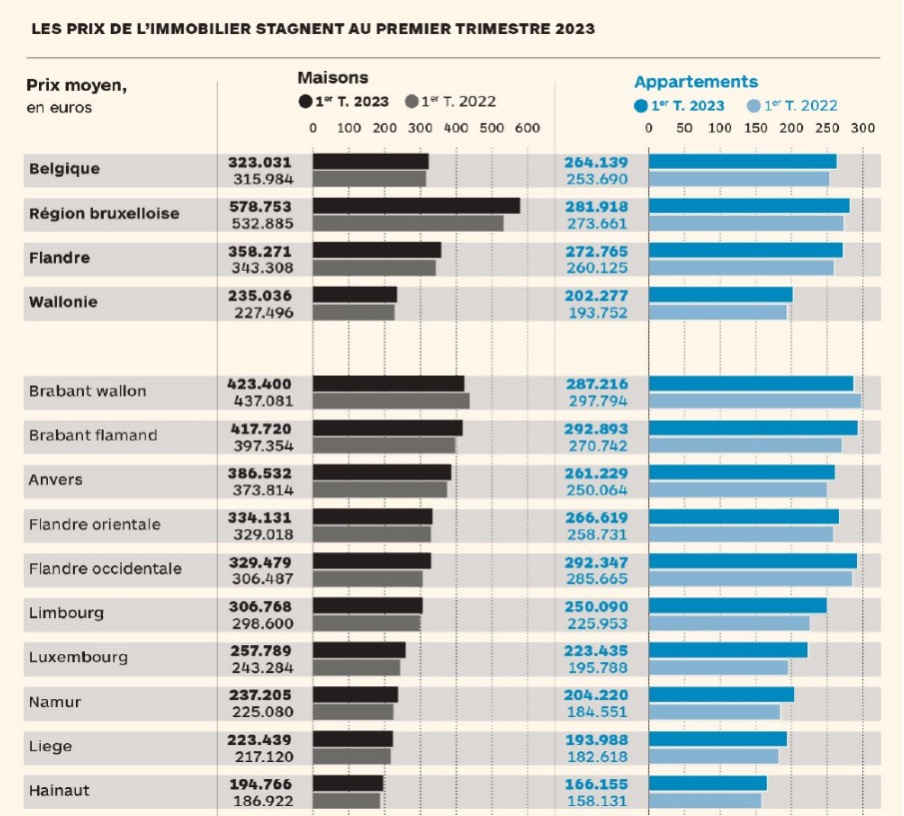

- The average price of a house in Belgium now stands at EUR 323,031, up 1.1% on the average for 2022 and 2.2% on the last quarter of last year. But in real terms, i.e. taking into account an average inflation of 7.11% in the first quarter of 2023, the price of this house has fallen by 4.91%.

- It is still in the Brussels Region that properties are most valued: a house costs EUR 578,753 (+8.6% in one year but +1.49% in real terms year-on-year and +0.8% compared to the average for the whole of 2022). In Flanders(EUR 358,271, -2.81% in real terms), prices are falling in real terms, as they are in Wallonia (EUR 235,036, -3.81%).

- Finally, the average price of an apartment in Belgium stands at EUR 264,139 (+1.5% compared to 2022 but -2.99% in real terms), with still significant regional disparities: EUR 272,765 in Flanders (-2.25%), EUR 202,277 in Wallonia (-2.71%) and EUR 281,918 in Brussels (-4.11%) for an apartment.

On the field, a correction in the order of 10% to 15%

What to make of these figures? Although they allow us to take the temperature of the market from a global point of view, these figures, compiled 4 times a year by the country's notaries, deserve to be refined: they reflect a price negotiated between buyer and seller sometimes more than 6 months before the deed of sale (a delay of half a year compared to the current market sentiment) and say nothing about the neighborhood where the "average property" is located, nor about the energy efficiency of the properties sold, for example, which is a criteria that is weighing more and more heavily on prices.

At BuyerSide, we have noticed that the type of properties we are looking for for our clients (mostly investment properties, with or without renovations, and located in quality neighborhoods) have seen their prices drop between 10 and 15% since last year and that these prices now seem to be stabilizing at this level.

After having to deal with a period of strong undersupply, buyers are taking back control, and this correction is making it possible to increase their gross yield to 4.5% (excluding capital gains) thanks to automatic rent indexation, compared to 3.5 - 3.75% last year. For a buyer, the negative impact of the rise in rates is therefore partially offset by the lower prices he or she can find on the market.

This yield has increased especially in the country's major cities. Per square meter, prices are now around 4,000 EUR/m² in the good neighborhoods of southern Brussels (Uccle, Ixelles, Watermael-Boitsfort, Auderghem, Woluwe, etc.), while prices in the municipalities on the other side of the canal (the municipalities of the northern crescent from Anderlecht to Evère) remain at 2,500 EUR/m².

Peak rates reached in September?

The market's downturn is therefore essentially due to the monetary tightening of the European Central Bank (ECB) which, like the Federal Reserve (Fed) in the United States, has gradually raised its key rates to curb spectacular inflation, pushing the yield on the Belgian 10-year Olo to more than 3% today whereas it was still in negative territory between 2019 and 2021.

As a result, the average mortgage loan is now over 4.5% for a 20-year fixed term in the windows of Belgian banks, a level not seen since October 2011, and which largely explains the drop in the number of applications processed.

In concrete terms, this means that an investor wishing to borrow EUR 500,000 will have to repay EUR 3,150 per month compared with EUR 2,466 per month a year ago (posted rate of 1.75% on average at the beginning of 2022), i.e. an additional cost of EUR 683.

But on closer inspection, the investor has good reason to be pleased :

- First of all, these are posted rates. In reality, each credit is unique and the borrower always has a margin of negotiation depending on the equity he brings to his project, his overall income, the purchase of ancillary products from his bank, his history with it, the ILL score of his investment, etc. Taking into account all these elements, the rate actually granted on average is 3.27%.

- Faced with this gap in the demand for credit, the banks have to fight harder to attract their customers and this competition is already reflected in their rates since, based on the Olo which has risen 300 basis points in one year, they should be around 5%.

- Inflation, after having reached 9.59% in 2022, should reach 3.9% in 2023 and 3.3% in 2024 according to the Planning Bureau. This means that, through the indexation mechanism, the borrower's monthly bill will be even lower. In our example of a EUR 500 000 loan, this means a "discount" of EUR 227 per month by the end of 2024 for the borrower, i.e. one third of the surplus imposed on him by the rise in mortgage rates.

- While the market agrees that the rate hike is not over because core inflation (prices of goods and services excluding food and energy) remains too high in the eyes of central bankers, the consensus already sees a possible inflection point emerging as early as September so as not to stifle the recovery (provided that this core inflation follows a sufficiently downward trend)

- Fewer borrowers on the market means, of course, fewer buyers. They will have less of a fight on their hands to get the investment they want and, as the Q1 figures show, will be able to benefit from better prices.

- Finally, for people wishing to invest a large part of their available equity in real estate, this is the perfect time. They will not be impacted, or only slightly impacted, by the rise in interest rates and will benefit from the fall in prices. If rates fall later, they can increase their debt exposure to recover equity to invest in other projects.